The bushfires have steadied, the fires that were out of

control are now under control, if not now largely all extinguished. It is now

time for the long road to recovery. Many endless hours of insurance assessing,

demolition of existing destroyed properties, delays due to contaminated waste

(older house with asbestos), thousands of kilometres of fencing to be erected

and then time to rebuild the properties and in some cases the rebuild the stock

numbers and lost fauna.

Yes, it all seems gloomy, but it is progress.

Yes, it will be slow, and frustrations will be vented. Due

in part to the apparent lack of speediness by the various people involved in

this complicated process.

Hold in there.

The world is in damage control with the coronavirus outbreak

(COVID-19) that appears to have it origins and ignition point in Wuhan, China

at Christmas 2019. Now rapidly spreading across the globe to have now impacted

some 80,000 + people.

Why all the doom and gloom, especially from a quantity

surveyor holed up in the comfort of his office.

I mean the content of this article thus far is not exactly

screaming “positivity or would be used at an inspiration seminar”.

Perspective people, perspective.

I wanted to make you aware of a word……. Embargo.

Noun

an

official ban on trade or other commercial activity with a particular country.

“an embargo

on grain sales”

verb

impose

an official ban on (trade or a country or commodity).

“all

of these countries have been embargoed by the US”

Sure, I would think you have heard about this term before.

Within the example used in the Noun above, it is not just applied or used on

grain sales.

To revert back to the opening line of this article, “The

bushfires have steadied……”.

Did you know that many of these areas that were engulfed by

fire and destruction had been, well, there was an embargo in place on property

insurance in those areas?

That’s right, it is a very common practice that insurance

companies and insurance underwriters will place an embargo on a particular

postcode or geographical area if they believe they are exposed to massive loss.

This is not to say that if you already have insurance in

place that it is void, however it does mean that should you not have insurance,

or you have let it expire, they very well may not allow a new policy to be put

in place on your property. In some cases, you are not even allowed to amend

your already current insurance policy.

As an example, if you have an existing policy and you have

just erected a new metal shed / garage in the backyard, you should consider increasing

your policy or add it to your policy. If the area was embargoed, you may very

well be under insurance as it may not be included for a period of time.

What is the reason for today’s article?

As Benjamin Franklin famously once said,

“Don’t put off until tomorrow what you can do today”.

It may well be too late if a storm is on the way or a fire

is ranging toward the back fence or water lapping at the street frontage.

An embargo restriction applied by an insurance underwriter

may be placed on a geographical area simply based on the fact that the

insurance underwriter believes that an area, or areas, is extremely likely to

be impacted. Not always that it IS ACTUALLY being impacted, but likely

to be.

I guess an example here would be a cyclone warning and a

projected path.

The embargo or restriction on an area usually comes with a

timeframe, which would seem logical, for example 72 hours or 7 days.

From the insurance underwriter perspective, in the past,

they have been exposed to scenarios where a client does not have any insurance

in play, however when a warning of an event or as an example a cyclone or

bushfire is on its way, take out an insurance policy.

After the threat has past, make additional contact with the

insurance underwriter and cancel the policy.

Embargoes on insurance are a normal and accepted practice,

and usually apply to new policies. They typically take effect when events such

as fires, floods and cyclones threaten to impact a certain area (or already

are). However, these embargoes can be across all forms of insurance as home,

contents, motor, business and travel.

If an insurable risk is imminent, the probability of that

risk occurring and therefore a claim being lodged is consequentially elevated.

Insurers, operating prudentially, would need to calculate a premium that

reflects this elevated risk, rather than averaging the risk over an entire

year. This would typically make a risk based premium unaffordable to a homeowner.

Not all insurers impose embargoes.

Australia’s insurance market is large and highly

competitive, and at any one time there are usually insurers who have not

enacted an embargo.

How to avoid being caught out by an embargo?

Make sure you have insurance in place all the time. Ensure

that your cover has been taken out well in advance of disaster season for your

location and avoid allowing it to lapse. Summer is a big part of the disaster

season here in Australia, generally speaking. We have most of our rainfall and

bushfires in the summer months.

However, think about your location, for example the tropical

North of Australia will have periods of high chance of increased rainfall (wet

season) and cyclones (storm season). Toward the alpine areas of Australia,

winter is also going to be a period concern with high snowfall.

Anyone in Melbourne should be on high alert ALL YEAR.

On any given day it could be raining, sunny, windy, snowing, cyclonic, raining

again, windy and cold.

As an example of what you can do to be more aware of these

weather activities and potential embargoes, I was doing some research and came

across a great website.

Early Warning Network Website

http://www.ewn.com.au/

Some of the services that they note on the website include:

- Location Based Warning Systems

- Local weather outlook

- Situation room

- National significant weather threat map

- Commercial location alerts

- Regional alerts

- Insurance embargoes

- API

- Flood monitoring and Warning

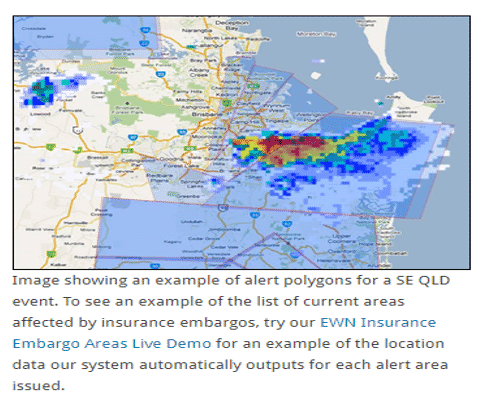

On the Early Warning Network website, it shows the areas

where embargos are in place. As an example, it would look something like this.

In addition to this, I would suggest that using the ICA

website is a good practice.

The Insurance Council of Australia has some great content on

the website and will help you regarding finding an insurance underwriter that

is willing to provide you cover even in an embargo.

In addition to this, they also provide data on the health

and trends in the insurance market.

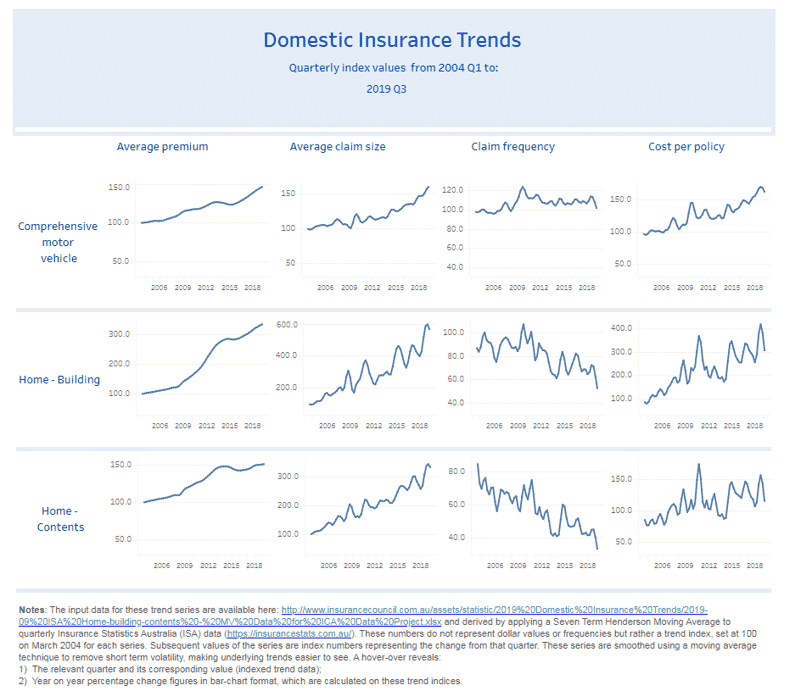

A snapshot of the Domestic Insurance Trends from 2002

Quarter 1 to 2019 Quarter 3, Is shown below:

You can see the average claim size for ‘Home – Building’ has

been steadily increasing from well below the $200,000 mark in 2004 to now well

over the $600,000 mark in 2019.

Either our homes are getting more expensive to build, or

more of the house is being impacted in the event, moving more toward total loss

rather than partial damage.

The next graph along from that is the claim frequency, which

will after the most recent events of bushfires and floods be taking a hike northward.

Since the 8th November 2019 through to now, a

reported by the Insurance Council of Australia, some 13,750 bushfire insurance

claims have been lodged, totalling damages of $1.34 billion.

An article in the Guardian Newspaper as of around the 14th

January 2019 this year, noted that both Suncorp and IAG, two of Australia’s

biggest insurers had a combined 67 embargoed areas on their books.

I know I have been on my soapbox regarding underinsurance and inaccurate use of website calculators over the years, however, it seems that the industry just did not have a voice. It appears since my rants have become more public; the supporting voices are now coming out of the woodwork.

Like Jonathan Brown of the consumer group Choice.

“Like all insurance decisions, that’s entirely up to you.

You need to carefully consider your own circumstances and look at independent

advice beyond calculators provided by insurers and commercial brokers or

websites”, says Jonathan Brown.

And now, even Campbell Fuller of the Insurance Council of Australia

(ICA) has publicly announced on the ABC that:

“About 80% of insured property owners are probably under

insured”, says Campbell Fuller of the ICA.

That was a direct quote from my last article on the inaccuracies of the online calculators within the industry. So, thank you, Mr Fuller.

For the residential property owner or homeowner, there is really

two types of insurance that you can take out on your property.

- Total Replacement Cover, and

- Sum insured cover.

The sum insured value will cover you up to the set amount

you choose to repair or rebuild your home.

So, in this circumstance, in my opinion, YOU MUST use the

services of a quantity surveyor to determine what the rebuild cost will be.

However, Jonathan Brown of the consumer group Choice,

further notes recently that:

“Some of the worst clauses allow insurers to base payouts

on the rates they can purchase materials and labour at, rather than the actual

cost of rebuilding or repairing your home”

“It may be worth considering a total replacement policy”

Mr Brown says.

As I have said before, know your numbers. The fine print on

policies do mean something and are worth your time.

Without being absolutely risk adverse on everything in life,

I believe that from time to time, it is worth taking into account the worst

that can happen in any particular scenario, then move backwards eliminating the

risk or putting things in play to reduce the risk.

Let’s keep positive people, outstretch that arm and hand of your and help someone that could do with the help. It is not just property, lives and animals that were lost in the brutal bushfires recently. Communities have been as well. Let’s all do what we can. Travel to these affected areas, if nothing else, spend our money locally to them to help to rebuild these communities.