If

we compare the number of homes that commenced construction in 2018, compared to

2019, 2018 wins. In fact, the total number of homes that commenced construction

in 2019 was 174,246.

The

total number of new homes that commenced construction in 2019 was 22.6 percent

lower than in 2018.

So,

over the full year, 2019 was not as great as the previous year. However, as an

industry, we had a lot to deal with.

Within

the property sector, there does seem to be headwinds in some way, shape, or

form each year. 2019 had it’s fair share though. We had the Financial Services

Royal Commission handed down its findings, the Australian Prudential Regulation

Authority (APRA) started the year with a firm hold on the industry, Federal and

state elections were held.

Earlier

in 2019, Geordan Murray, the HIA Senior economist had said, tax changes on

property ownership, such as the opposition Labor Party is promoting ahead of

the May 18 federal election, would only make the situation worse.

“State

and federal governments should be looking at ways to sure up confidence in the

housing market, for both owner-occupiers and investors,” HIA senior

economist Geordan Murray said.

Then,

on the 21st May 2019, APRA, the banking regulator, proposed

relaxation of lending restrictions.

Coupled

with the Reserve Bankrolling out two consecutive interest rate cuts. Surely

this would start to see the 2019 year improve. Surely this was the road back to

recovery.

Martin

Farrer, of The Guardian, published on the 16th November 2019, What

has caused the turnaround?

In

his opinion, CREDIT.

“The

simple answer is credit. Just as the downturn was caused by Apra’s 2017

decision to restrict credit amid alarm about

poor lending standards, the upturn has coincided with a loosening of credit

restrictions”.

The

founder of SQM, Louis Christopher, says Apra’s post-election U-turn was

crucial.

“With

Apra, what they really did was, someone, knocked on their door and said, ‘Look,

you’ve gone too far, we’ve got a downturn in the economy, you’ve got to loosen

the lending restrictions.’ And they did.”

The

second half of 2019 showed a marked improvement in housing market sentiment with

suggestions that demand for new homes would return to growth going into 2020.

This

month, on the 15th April 2020, The ABS released building activity

data for the December quarter of 2019, rounding out the full calendar year

results.

Maybe

we are back on track. In December 2019, leading indicators of building activity

that showed an improvement in new home construction, there was a 1.2 percent

increase in new home construction in the December quarter.

“There was a small increase in the number of

new homes that commenced construction in the December quarter,” said Angela Lillicrap,

HIA Economist.

“This

quarterly increase at the end of 2019 was reported in both detached dwellings

and multi-units, increasing by 0.1 percent and 2.9 percent respectively.

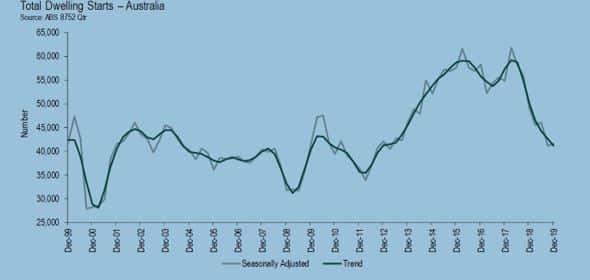

With December 2019 showing the number of new homes starting

construction being just above the 40,000, we had not seen these low numbers

since December 2013. With December 2017 being between the 55,000 and 60,000

mark numbers.

As we moved into the new year, a decade even, building

approvals were on the rise.

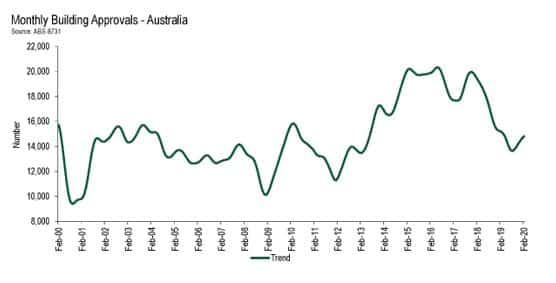

“Building

approvals increased by 3.9 percent in the three months to February 2020

compared to the previous three months, providing further evidence that the

housing market was accelerating into 2020,” stated HIA Economist, Angela

Lillicrap.

“Approvals

strengthened across the board with both detached houses and multi-units

experiencing quarterly increases of 2.9 percent and 5.4 percent respectively.

From

this, we know that up until at least the end of February, home building

activity across most regions for 2020 was looking at the improvement.

In

seasonally adjusted terms, building approvals for the three months to February

2020 quarter showed:

Victoria

(+22.6 per cent),

Western

Australia (+1.1 per cent),

Tasmania

(-7.3 per cent),

New

South Wales, (-5.2 per cent),

Queensland

(-4.9 per cent),

South

Australia (-17.4 per cent),

Australian

Capital Territory(+ 1.0 per cent), and

Northern

Territory (- 6.7 per cent.).

From

this, what I see is that we have a property market on the improvement. Then we welcome

COVID-19 to our shores. Although we lock the door and do not want it to enter,

it comes in anyway.

With

various stimulus packages being rolled out, Government incentives to encourage

support and continued employment, it is fair to say that the construction

industry is still open for business.

The

Australian Government was pledged $1.3 billion to support keeping apprentices

employed, by way of a $21,000 per apprentice subsidized wage.

A

month ago, HIA Managing Director, Graham Wolfe, said,

“The

measures that the Government has announced will help many small businesses

continue to operate in this uncertain environment.”

“As

an industry that employs over 1 million people and injects billions into the

economy, the residential building industry can play a key role in keeping the

economy ticking over and lead the economic recovery that will happen once the

virus passes,” concluded Mr. Wolfe

As

I had noted earlier, one of the key drivers for the change from early to mid-2019

has been credit, or the ability to gain credit.

We

now have more headwinds. 2020 is no different. It is not a royal commission, or

a federal election, but a worldwide pandemic.

However,

if the industry has access to credit and can continue to build, then we have a

chance.

The

value of lending to owner-occupiers (construction of new homes) in January 2020

has increased to 13.2 percent higher than back in April 2019.

Written by Marty Sadlier

Founding Director and Owner at MCG Quantity Surveyors