As part of the services of quantity surveyors, we are regularly commissioned to undertake progress claim assessments on behalf of financial institutions.

During the last month, we have seen quite a common conversation held between ourselves and a client (developer) regarding the difference between our assessment of the builders claim and the amount that the builder was claiming for.

It will be no surprise to many of you, our quantity surveyors assessment of the builders claimed amount was less than that claimed for by the builder.

Are we harsh, or is this a reflection of two different methods of assessment and claiming for works completed to site?

It is the latter.

In the scenarios that I am referring too last month, we had four (4) builders indicate to ourselves and the developer that they would be ceasing works on the site until there progress claim had been paid in full.

In these instances, the builders had submitted their progress claims as per the signed construction contracts, as Staged Progress Payments or Milestones.

These contracts were either Master Builders Association contracts (MBA) or Housing Industry Association contracts (HIA).

The builder will nominate percentage values to each of the stages, with a common break up being:

Deposit – 5 %

Base stage – 10 %

Frame stage – 15 %

Lock Up stage – 35 %

Fixing stage – 25 %

Completion – 10 %

Total – 100%

From the client or developer’s perspective, they had sought funds from a financer, which was based on the release of funds being assessed by a quantity surveyor and based on ‘works completed to site’.

In these four (4) scenarios, there were two (2) reasons for the difference in the assessment of the progress claim value.

The percentage nominated as being completed to site ‘Frame Stage’ was much higher than the value of the works completed to site.

Works had not been completed to site that fulfilled the definition of the milestone.

In the issues surrounding the overstated percentage for a particular milestone (Point 1), the percentage of the contract value that is claimed each time is not a reflection of the actual works completed to site. The builder will have increased the value of each of the stage percentages so that they can fund deposits and long-lead materials for the future works and stages. For example, with the 10% of the base stage funds claimed, so of those funds will be used for the securing of timber wall and roof frames deposits and window deposits.

The risk to the client is that in the event of the Builder or building company going under or leaving the project, there may or may not be enough funds left to successfully finish the project.

However noting this, the construction contract that notes milestones is still a legally binding document.

Therefore, in these cases, the discrepancy between the claimed amount and the assessed amount has forced the client to put their hand in their pocket to make up the difference between what the financier will pay and what is written in the building contract.

This shortfall of funds will take some time for the client to get to the builder, in turn, delaying the program by a few days.

With the scenario of point 2, although our assessment of the works was based on works completed to site, the client was not required to pay the builder any funds as they had not completed the works as defined in the contract as being required to fulfill the milestone.

The builder had claimed for ‘Fixing Stage’. The contract defined fixing stage as:

Fixing Stage – “means the stage when all internal cladding, architraves, skirting, doors, built-in shelves, baths, basins, troughs, sinks, cabinets and cupboards of home are fitted and fixed in position”.

However, freestanding baths had not been placed in position and basins had not been installed to the stone benchtops on some of the vanity units.

In this scenario, the builder really should have considered the types of fixings and fittings specified for the development and considered modifying the wording of the milestone or moving some of these items to the final stage definition.

It is no secret that obtaining finance is still a stumbling block for developers in the current economic climate, so our advice is that understanding the constraints and potential funding issues that a development may face is absolutely paramount.

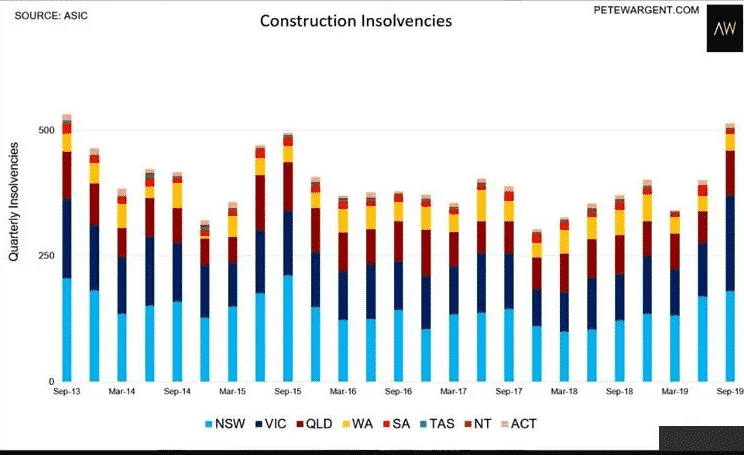

New figures show the housing slowdown is biting NSW hard, with the number of construction companies going under last quarter hitting its highest level in almost four years.

Statistics provided by ASIC show 169 NSW-based construction companies went into administration, receivership or a court-ordered shutdown in the June quarter. This is the highest number since the September quarter of 2015.

Over the whole 2018-19 financial year, 556 construction companies went under — 101 more than the previous financial year.

Mr. Hathway, Association of Independent Insolvency Practitioners president and who also runs his liquidation firm, said small construction companies had been hit hardest.

Stephen Hathway said there was no doubt the industry was “stressed”. “These days it’s subcontractors on subcontractors,” he said.

“And the general feel I’m getting from talking to my fellow liquidators, is that in the building industry subbies just slow down paying the little ones (construction companies).

Sure, there are various reasons why construction companies fail. However, cash control and the timing of funds coming in are a major contributor to the issues.

More and more reason to be fully aware of how funds are to be paid to you by either a developer or financier.

Understanding the potential pitfalls or bottlenecks pertaining to progress claim funding will allow builders and developers to avoid exposing themselves to these risks.

Written by Marty Sadlier.

Marty is a property investor, cost estimation specialist and Director of MCG Quantity Surveyors. His passion is ensuring that developers and investors alike gain a comprehensive understanding of all construction costs and potential risks on their developments. Marty’s mission is to assist property developers to achieve financial security through accurate construction consultancy services. You can visit them at www.mcgqs.com.au/