Coronavirus creates the most competitive building environment since the GFC

A study by MCG Quantity Surveyors has revealed property owners are now securing the most competitive building and renovation environment in almost a decade.

MCG Quantity Surveyors were recently featured in the Australian Financial Review on the back of their recent analysis of construction contracts prompted a survey of builders which revealed most are dramatically reducing quotes to secure work.

We believe the coronavirus crisis has opened a window of opportunity for property owners to make substantial savings on building costs, but it has the potential to close just as quickly, so you must stay on your toes.

The last time that we really were witness to such a dramatic correction in the market was during and after the global financial crisis (GFC). It was after the GFC a committee was formed to examine the impact of change on regional Australia and test policy responses.

The current environment bore similarities to what we saw during the GFC apart from one major difference. During the GFC it was difficult to determine how long it would take for confidence to return and the fallout ran for many years afterward.

With the current crisis, it’s more likely that the relaxation of restrictions and perhaps a medical solution will boost confidence quickly.

At the request of the Parliament of the Commonwealth of Australia, titled “the Global Financial Crisis and regional Australia”, formed the Standing Committee on Infrastructure, Transport, Regional Development & Local Government. The findings recommendations and responses were released in November 2009.

The Chair, Ms. Catherine King MP, noted within the forward, “The GFC should be seen as an opportunity to. The lessons learned will assist in strengthening existing regional development policy, which will help regional Australia withstand future downturns.”

The Committee reported on the evidence it received, noting the effects of the crisis, the key sectors reviewed were:

- Resources;

- Manufacturing;

- Tourism;

- Retail;

- Construction;

- Primary industries; and

- Banking and lending.

From a quantity surveying perspective, focus pertaining to the construction sector has been of most interest, with an attempt to compare the GFC to that of the potential fall out of the COVID-19 pandemic currently tearing its way across the globe. Have we learned anything from the GFC that can be applied by way of focusing our vision?

The committee’s findings from the review of the GFC found that perhaps more than any other sector of the economy, the construction industry can be ‘notably affected by the economic cycle’, in particular the economic conditions created by the GFC.

It was concluded by the committee that the lack of available credit at the time impacted heavily geared sectors such as commercial and medium-density property construction, coupled by the declining output from the nation’s mines, factories, office blocks, and shopping centers means that the ‘incentive to construct additional capacity is weak’.

Does this not at the very least present a similar landscape to the one we find ourselves in currently?

Okay, a global pandemic is not the same as “the residential housing bubble, Bursting”, but are we not going to have to claw our way back out of the doldrums after the COVID-19 annihilations of the Australian construction sectors. Are they not going to be similar in terms of the long road to recovery?

As a point of reference, let’s refer to the ‘Producer Price Index’. The PPI is a “price index that measures the average changes in prices received by domestic producers for their output. Its importance is being undermined by the steady decline in manufactured goods as a share of spending”.

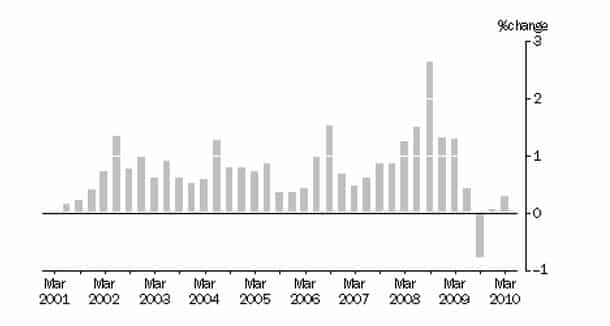

What can we learn from the PPI of the materials used in house building at the end of the March Quarter in 2010?

The Australia Bureau of Statistics (ABS) indicates that the price index of materials used in house building increased by 0.3% in the March quarter 2010.

This followed a 0.1% increase at the end of the December quarter 2009.

A decrease of 0.8% in the September quarter 2009

MATERIALS USED IN HOUSE

BUILDING, All groups: Quarterly % change

The graph shoes the crescendo of price increases in the midst of the GFC, the decline toward the end of the GFC with the negative result at the end of the September quarter 2009.

It is this PPI analysis post-GFC that should be of interest to the Australian Construction Sector in 2020-2021. Post COVID-19, construction will once again recommence across the country without isolation and the shackles of the pandemic.

We are working with builders now where we simply can’t get to their costs under the usual analysis. For example, we have a builder who we are constructing a residential unit development for $2.5 million, and our QS assessment, based on their usual rates for the same type of development 8 months ago was $2.8 million.

It’s fair to say that if you had a building contract priced and quoted 12-months ago and then had that same contract priced today, the 2020 amount to build would be much less.

MCG Quantity Surveyors surveyed builders with whom we’ve had a business relationship and the results show owners ready to seek a quote from a builder have been handed a golden opportunity to get maximum construction bang for their buck.

There will be an approach to ‘make up for lost time’, a capacity to achieve a full roster of labor and programs of work.

Instead of waiting the many months to secure a tradesman, whilst only being able to even contemplate selecting from a select few, there will be a plethora of sub-contractors for all trades.

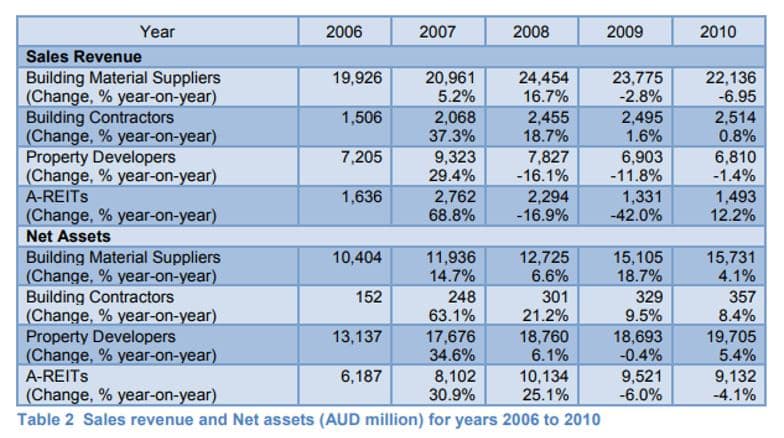

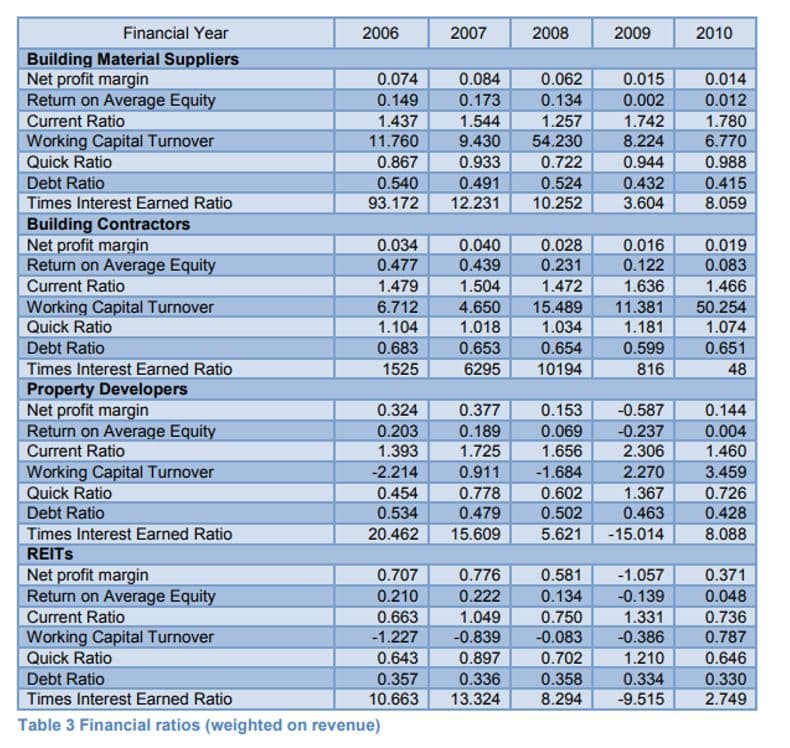

Post GFC, Ram Karthikeyan Thangaraj, and Toong Khuan Chan (The University of Melbourne, Australia) published a paper titled “The Effects of the Global Financial Crisis on the Australian Building Construction Supply Chain”.

This study involved a financial analysis of 43 publicly listed and large private companies in the building and construction supply chain from 2006 to 2010.

Interestingly enough, albeit the stimulus packages implemented to support builders and material suppliers were rolled out, toward the end of the GFC and into 2010, Sales revenue and net assets for both materials suppliers and building contractors started to fall.

Whereas, the Real estate had started to improve in terms of sales revenue.

When comparing the net profit margins of these same 4 sectors, building material suppliers were the only sector to decrease in net profit margin year on year.

In terms of profitability, the net profit margin (net profit divided by sales revenue) for material suppliers reduced progressively from more than 7% in 2006 to 1.4% in 2010.

The net profit margin for building contractors was low at between 3.4% in 2006 and reduced to a minimum of 1.6% in 2009. It recovered slightly to 1.9% in 2010.

The net profit margin for property developers was more than 32% before the onset of the GFC, then fell through the floor to reach -59% loss in 2009.

Covid-19 is having an impact on the construction sector, inevitably for some further time to come. The landscape will be vastly different from what we have seen over the years 2014 to 2017.

When taking this conversation directly to a developer in April 2020, Melbourne based developer Mr. Tom Howgate of Kincrest, indicated that the headwinds are not funding availability, however councils increasing open space contributions and the whole environment becoming hyper-competitive, very quickly.

MCG Quantity Surveyors sent a series of questions to nine builders with experience in projects from large scale commercial and residential ventures through to new-home builds and renovations.

The summary of the opinions was unanimously centered around the decline in construction costs and was attributable to four (4) elements:

- Workflow’s rapidly declined

Around half of the builders have seen their work pipeline halt.

While some have projects locked in for the rest of 2020, just under half the builders had projects nearing completion and they’re struggling to secure new work. Some have also had to halt work due to social isolation rules. Some builders have clients under financial stress who have needed to shelve their project with hopes of picking up again once the crisis has passed.

This was also evident with builders looking after mum-and-dad home projects, they also had found their work drying up.

When owners are out of work, finance becomes a major headache and some have put a stop to builds that are already underway. This has seen a rising number of builders finding themselves back on the market.

- Margins being cut

We found that builders are now willing to sacrifice their profit margins in order to keep their business operating.

In the current environment, builders are looking to simply keep going in anticipation of better days, and many are willing to ‘work for free’ in order to keep the doors open.

This was made most apparent given seven of the nine I surveyed confirmed they were planning to, or had already, cut their margins in order to win work. Despite this, some were already losing work to others quoting at below cost price.

- Subcontractor rates plummet

Subcontractors were slashing their hourly rates so as to keep jobs.

All nine builders said their subcontractors are becoming hyper-competitive. The builders expressed that they had never seen an environment like this where highly-skilled and sought after tradesmen were hungry for work.

“It’s no longer ‘can I find a tiler” because they’re all booked out. Now you’re going to have your pick of every tiler in the country”, said one builder.

“Subbies who are already on the builder’s books are cutting their rates to stay in with their head contractors, while new subbies are increasingly making contact looking for work”, said another.

This has been exacerbated by the shutdown of major projects where subcontractors thought they were locked in with employment for the next year or two. Many of these jobs have been shuttered and there’s now a flood of subbies looking for employment.

This means that head contractors are able to secure subcontractors at extremely competitive rates, and those saving are being passed on to customers through lower quotes in an attempt to win work.

- Cheaper materials

Builders also expressed that certain building materials have become more affordable to the source.

The general consensus is that for staples such as floor coverings or brickwork, suppliers are now more competitive, but specialist items such as light fittings or imported finishes were less likely to see price drops.

Furthermore, there is no delay in sub-contractors getting quotes back into their builder clients. Where a subcontractor would need to be chased for a price and hounded, we are seeing quotes coming in hours or only a day or two.

Of course, timing is everything. The crystal ball moment is hard to define. Once those builders have filled their books with projects, you won’t get a builder to do your job.

Written by Marty Sadlier

Founding Director and Owner at MCG Quantity Surveyors