The ATO allows two very different methods of calculating property tax depreciation deductions, the Diminishing Value Method and the Prime Cost Method. Most investors choose the Diminishing Value Method as it will return the greatest amount of deductions over the first few years of ownership. However it’s worth discussing with your accountant, as maximising your claim upfront might not be beneficial if your income is likely to increase substantially down the track.

Let’s take a look at some of the key differences between the Diminishing Value and Prime Cost Methods.

| Diminishing Value Depreciation Method | Prime Cost Depreciation Method |

|

|

Both methods of depreciation claim the same total value over 40 years. However, they utilise different rules to achieve either aggressive upfront claims or a more consistent claim each year.

For example, consider an asset like carpet, worth $18,000 with an effective life of 10 years.

So for year one;

The calculation to reach the depreciation rate for the diminishing method is 200 divided by the effective life. So, 200 / 10 = 20%

The calculation to reach the depreciation rate for the prime cost method is 100 divided by the effective life. So, 100 /10 = 10%

In subsequent years, the calculation for the diminishing method becomes more complex, whereas prime cost stays the same. Prime cost will be 10% of $18,000 until all of the value is claimed after 10 years, so $1,800 every year for 10 years.

The diminishing method needs to subtract the value of the previous year(s) claim, before working out the deductions for the current year. So for year two the calculation is;

Opening Value ($18,000) minus year 1 claim ($18,000 X 20%, or $3,600) multiplied by 20%

This equates to;

$18,000 – $3,600 = $14,400 then;

$14,400 X 20% = $2,880.

Year three will then be ($18,000-$3,600-$2,880) X 20%. This will give $2,304.

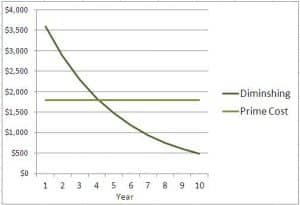

When represented in a line graph, you can clearly see the result of the diminishing method and its decreasing deductions, verses the constant deductions of the prime cost method.

The line graph is useful as it shows the point at which the diminishing method of claim ceases to produce higher deductions than the prime cost method. In this 10 year scenario, the diminishing method wins out each year until year 5.

The point at which the two methods meet is different for each property as the mix of plant and equipment assets are different. As plant and equipment items have different effective lives, their depreciation percentages will be different. For example, ceiling fans with an effective life of 5 years, will be 40% under the diminishing method, and 20% under the prime cost method.

For information on how effective lives are calculated, you can visit here.

Property investors are usually keen to get the maximum depreciation deductions up front, and we’re often asked “why would someone choose the prime cost method?”

An investor who wants more of a guaranteed tax return amount each year would benefit from the prime cost method. As you can see from the line graph, the deductions are constant over a long period of time. Another reason might be someone purposely trying to minimise their deductions in the first few years of ownership. For example someone with a low income that is likely to have a much higher income later on. Finally there are property investors who occupy their property as their primary place of residence. A short 6-12 month stay might not make much of a difference, but occupying the property for 5-6 years most likely would.

The purpose of putting this article together other than giving a background into how the depreciation methods work, and how they affect depreciation claims over time, is to encourage you to look at both methods and talk to your accountant to ensure that you’re working with the method that’s most suitable for your scenario.